- 20 Marks

PSAF – Nov 2020 – L2 – Q2 – Preparation and presentation of financial statements for local government

Prepare financial statements (Statement of Financial Performance and Statement of Cash Flow) and explain basic disclosure requirements for Eminaa District Assembly.

Question

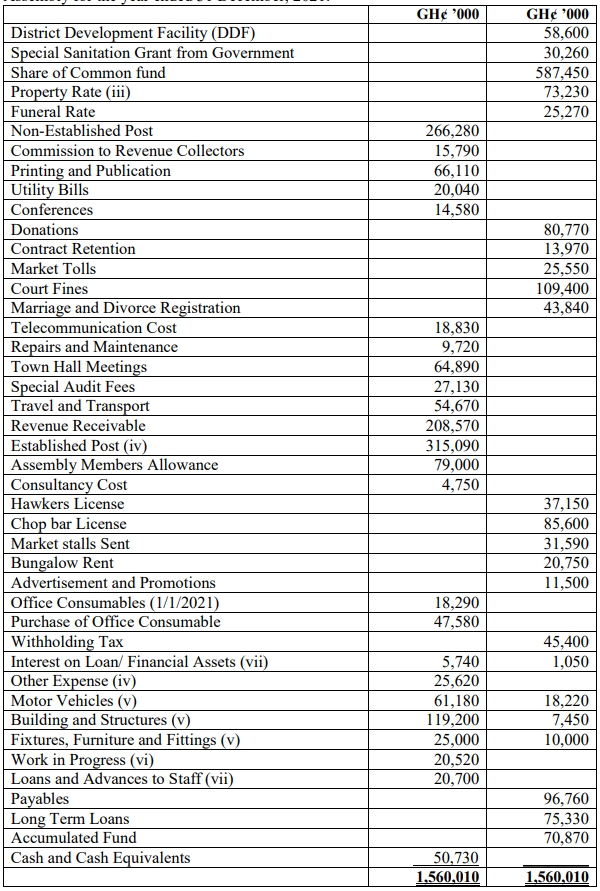

a) The following details relate to Eminaa District Assembly for the year 2018.

| Details | GH¢’000 |

|---|---|

| Dividend Received | 93,250 |

| Central Government Salaries | 12,000,000 |

| Basic Rates | 370,900 |

| Districts Development Facility | 15,000,600 |

| Rent from Land and Building | 6,120,800 |

| Established Posts | 1,140,700 |

| Other Expenditure | 600,000 |

| Non-Established Posts | 580,000 |

| Allowances | 390,470 |

| Court Fees | 240,000 |

| Inventory and Consumables | 800,000 |

| Sanitation Fees | 370,000 |

| General Cleaning | 350,000 |

| Common Fund | 2,930,000 |

| Social Benefit | 840,300 |

| Equity Investment Acquired | 420,000 |

| Infrastructure, Plant, and Equipment | 980,000 |

| Work-In-Progress | 490,000 |

| Loans Received | 2,330,000 |

| Interest Expense | 200,000 |

| Advances to Staff | 660,000 |

| Royalties | 430,000 |

| Consultancies cost | 470,000 |

| Training and Workshop cost | 275,000 |

| Transport and Travelling cost | 620,000 |

| Consumption of Fixed Assets | 960,000 |

| Special Services | 820,000 |

| Utilities | 630,000 |

| Market Tolls | 870,000 |

| Permit Fees | 990,000 |

| Fines and Penalties | 330,000 |

| Development Bonds Issued | 1,300,000 |

| Hostel License | 630,920 |

| Business Income | 2,300,600 |

| Chop Bar License | 300,400 |

| Proceeds from Sale of Equity | 990,320 |

| Accumulated Fund (1/1/2018) | 370,600 |

| Herbalist License | 530,370 |

| Cash and Cash Equivalent @ (1/1/2018) | 12,300,240 |

| Stool Land Revenue | 600,000 |

| Lorry Park Fees | 720,400 |

| Market Store Rent | 300,750 |

| Recoveries | 194,000 |

| Loan Repayment | 143,000 |

| Property Rate | 820,900 |

Additional Information:

- Eminaa District Assembly adopts the accrual basis of accounting in the preparation of its financial statements.

- Established Post salaries outstanding as at 31/12/2018 were GH¢180,000,000.

- Inventory at 31/12/2018 was GH¢170,000,000.

Required:

Prepare for Eminaa District Assembly:

- Statement of Financial Performance for the year ended 31/12/2018.

(7 marks)

b) Prepare a statement of cash flow for Eminaa District Assembly for the year ended 31/12/2018. (8 marks)

c) Subject to IPSAS 6: Consolidated and Separate Financial Statements, a Controlling Entity that presents Consolidated Financial Statements shall disclose certain basic information.

Explain FIVE (5) basic information that an institution preparing Consolidated Financial Statements needs to disclose. (5 marks)

Find Related Questions by Tags, levels, etc.

Report an error