Question

Answer

a) Put options are required to hedge the price of the shares.

Step 1: Determine d1 and d2

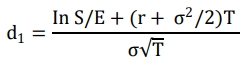

S = 360

E = 360 × 0.95* = 342

* The exercise price is 5% lower than the market price as that is the protection required.

r= 0.04

= 13% = 0.13

T = 6/12 = 0.5

Step 2: Determine N(d1) and N(d2)

N(d1) = N(0.8215) = 0.2939 + 0.15(0.2967 – 0.2939) = 0.2943

Since d1 is positive, we add 0.5 to get 0.5 + 0.2943 = 0.7943

N(d2) = N(0.7296) = 0.2642 + 0.96(0.2673 – 0.2642) = 0.2672

We also need to add 0.5 to get 0.7672

Step 3: Determine the value of call

![]()

Step 4: Using Put Call Parity (PCP), determine the value of put option

On the assumption that one put option is bought per share:

Total value of Option = 27.75 million × 3.99kobo = ₦1,107,225

Overcharge by bank: ₦1,250,000 – ₦1,107,225 = ₦142,775

b. How a Decrease in the Following Variables Affects a Call Option

i. Volatility of the Stock Price

- A decrease in volatility will reduce the value of a call option. This is because a lower volatility means a lower probability of significant price movement, reducing the potential for the stock price to rise above the strike price, thus lowering the value of the option.

ii. Risk-Free Rate

- A decrease in the risk-free rate will increase the value of a call option. A lower risk-free rate reduces the present value of the strike price (since e-rT becomes larger), making the option more valuable as it is cheaper to exercise the option in the future.