Question

Answer

(a) Implications of Change in Accounting Policy

Users of financial statements need to compare financial statements over time, consistent with the principle of comparability. A change in accounting policy, as necessitated by IAS 38, requires retrospective application:

- Training costs, now classified as expenses, cannot be capitalized as intangible assets.

- Retrospective application means adjusting prior periods’ financial statements and equity.

- For Likely Effect Limited, training costs capitalized in 2012 (N6m) and prior periods (N12m) will now be derecognized.

- This adjustment impacts retained earnings, reducing equity and altering profit figures for prior periods.

b. (i) LIKELY EFFECT LIMITED

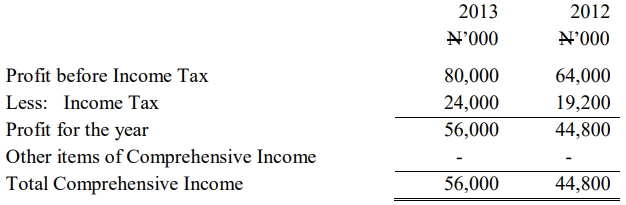

Statement of Comprehensive Income for the Year ended 31 December, 2013

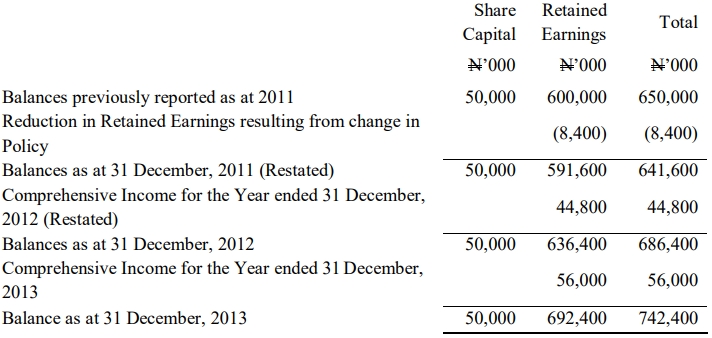

(ii) Statement of Changes in Equity for the year ended 31 December, 2013

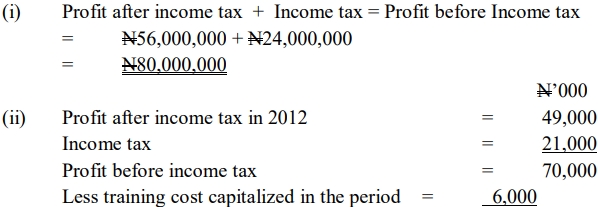

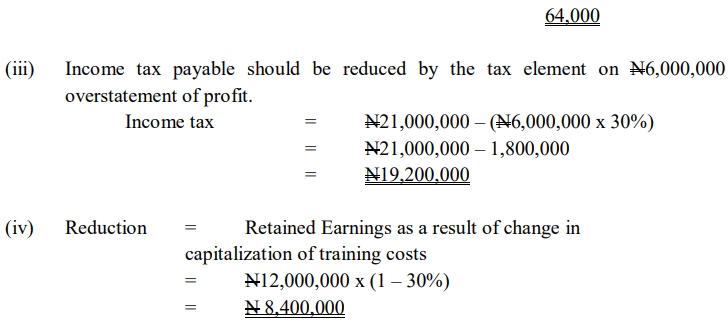

Workings:

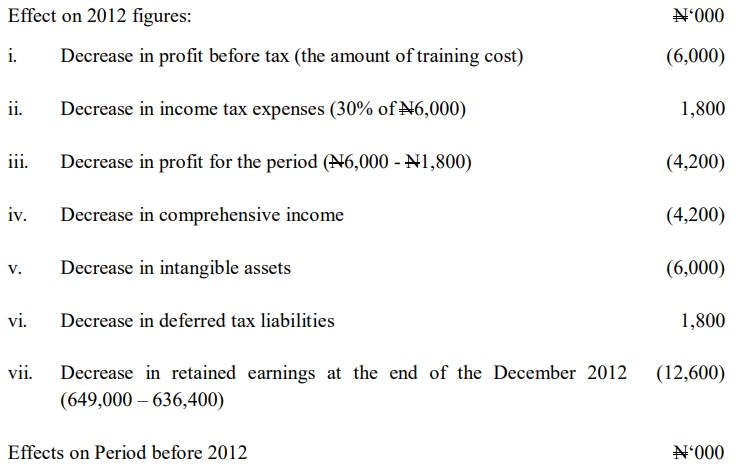

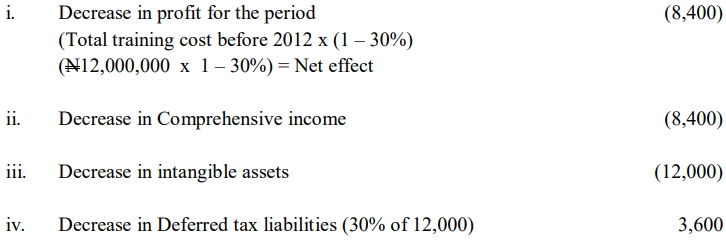

c. Effects of change in Accounting Policy on previous periods:

Apart from restatement of comparative figures for 2012 on the Statement of Comprehensive Income, the following items will be affected as analyzed below