- 16 Marks

CR – May 2021 – L3 – Q2b – Segment Reporting (IFRS 8)

Apply IFRS 8 principles to segment information and discuss disclosure requirements.

Question

The advisors of Amaka Limited have requested various types of information from the company to facilitate the preparation of a prospectus and other financial information in view of the fact that Amaka Limited is about to be listed on the Nigerian Stock Exchange.

As the Chief Accountant of the company, the CEO has requested that you provide the advisors with necessary information about your company that you use to allocate resources and assess performance of the company in year 2019.

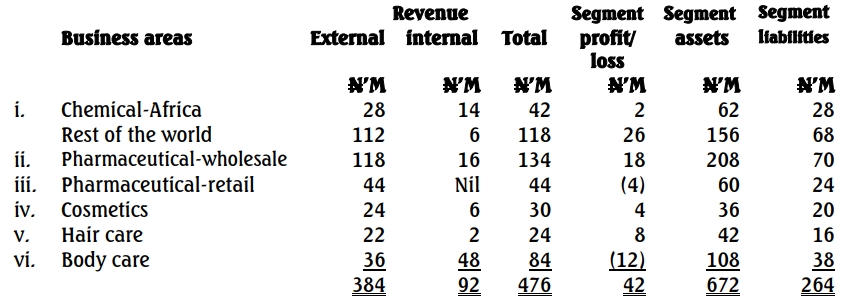

You have therefore identified the following potential segments that could be reported on, based on the areas of location of the company’s operations in West Africa.

| Location | Revenue (N’000) | Profit/(Loss) (N’000) | Assets (N’000) | Liabilities (N’000) |

|---|---|---|---|---|

| Gambia | 93,600 | 19,440 | 98,460 | 75,600 |

| Ghana | 25,200 | (7,740) | 14,400 | 13,500 |

| Nigeria | 317,340 | 21,240 | 258,210 | 74,970 |

| Togo | 41,400 | (1,440) | 21,600 | 14,400 |

| Total | 477,540 | 31,500 | 392,670 | 178,470 |

Required:

i. Explain how the principles highlighted in (a) above would be applied to Amaka Limited using the information provided. (12 Marks)

ii. Discuss other disclosure requirements which Amaka Limited should include in the financial statements for the year ended December 31, 2019 as required by IFRS 8. (4 Marks)

Find Related Questions by Tags, levels, etc.

- Tags: Financial Disclosure, IFRS 8, Operating segments, Segment Reporting

- Level: Level 3

- Topic: Segment Reporting (IFRS 8)