Question

a) Sandoo Ltd is a company which manufactures machinery for industrial use and has a year end of 31 December 2021. The directors of Sandoo Ltd require advice on the following transaction:

i) Sandoo Ltd acquired a cash-generating unit (CGU) several years ago but, at 31 December 2021, the directors of Sandoo Ltd were concerned that the value of the CGU had declined because of a reduction in sales due to new competitors entering the market. At 31 December 2021, the carrying amounts of the assets in the CGU before any impairment testing were:

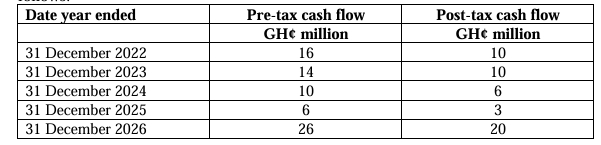

ii) The fair values of the Property, Plant and Equipment and the other assets at 31 December 2021 were GH¢20 million and GH¢34 million respectively and their costs to sell were GH¢200,000 and GH¢600,000 respectively. The CGU’s cash flow forecasts for the next five years are as follows:

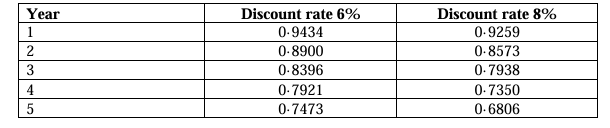

iii) The pre-tax discount rate for the CGU is 8% and the post-tax discount rate is 6%. Sandoo Ltd has no plans to expand the capacity of the CGU and believes that a reorganisation would bring cost savings but, no plan has been approved. The directors of Sandoo Ltd need advice as to whether the CGU’s value is impaired. The following extract from a table of present value factors has been detailed below:

Required: With reference to relevant International Financial Reporting Standards: Advise the directors of Sandoo Ltd on how the above transactions should be accounted for in its financial statements as at 31 December 2021.

(10 marks)