- 20 Marks

ATAX – May 2016 – L3 – Q2 – Petroleum Profits Tax (PPT)

Compute assessable and chargeable profits, assessable and chargeable taxes, and tertiary education tax for Sky Petroleum Plc.

Question

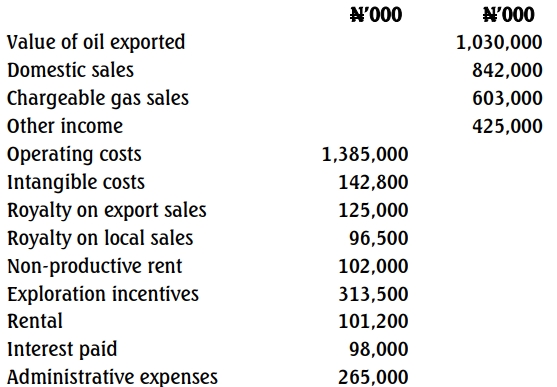

Sky Petroleum Plc commenced operations over ten years ago and makes up accounts to December 31 annually. The following details have been extracted from the accounting records for the year ended December 31, 2014:

| Details | Amount |

|---|---|

| Crude Oil Exported | 3,500,000 barrels |

| Crude Oil Used Locally | 1,200,000 barrels at ₦100 per barrel |

| Incidental Income from Petroleum Operations | ₦26,750,000 |

| Exploration and Drilling Costs | ₦30,000,000 |

| Management and Administration Expenses | ₦240,500,000 |

| Non-Productive Rents | ₦8,300,000 |

| Allowance for Bad Debts – General | ₦7,500,000 |

| Allowance for Bad Debts – Specific | ₦11,200,000 |

| Depreciation | ₦7,250,000 |

| Losses Brought Forward | ₦13,200,000 |

Qualifying Capital Expenditure:

| Asset | Date Acquired | Location | Amount (₦) |

|---|---|---|---|

| Pipeline and Storage Tanks | March 2014 | Continental Shelf (190m water depth) | ₦48,000,000 |

| Plant and Machinery | June 2012 | Territorial Waters (90m water depth) | ₦63,800,000 |

| Furniture and Fittings | May 2011 | Territorial Waters (95m water depth) | ₦21,000,000 |

| Building | April 2013 | Onshore | ₦71,000,000 |

Breakdown of Management and Administration Expenses:

| Item | Amount (₦) |

|---|---|

| Donations to Political Parties | ₦8,500,000 |

| Expenditure for Petroleum Deposit Information | ₦4,700,000 |

| Companies Income Tax of an Associated Company | ₦5,000,000 |

| Interest on Inter-Company Loans (at market terms) | ₦2,600,000 |

| Staff Salaries | ₦175,000,000 |

| Royalties on Export Sales | ₦6,200,000 |

| Repairs and Renewals on PPE for Petroleum Operations | ₦2,900,000 |

| Rents Paid for Oil Prospecting License | ₦3,600,000 |

| Other Administrative Expenses | ₦32,000,000 |

| Total | ₦240,500,000 |

Additional Information:

- International market price of crude oil in 2014 was USD $75 per barrel.

- Exchange rate: USD $1 = ₦280.

Required:

a. Compute the Assessable Profit. (11 Marks)

b. Compute the Chargeable Profit. (5 Marks)

c. Compute the Assessable Tax. (1 Mark)

d. Compute the Chargeable Tax. (2 Marks)

e. Compute the Tertiary Education Tax. (1 Mark)

Find Related Questions by Tags, levels, etc.

- Tags: Assessable Tax, Chargeable Tax, Petroleum Profits, Tertiary Education Tax

- Level: Level 3

- Topic: Petroleum Profits Tax (PPT)

Report an error