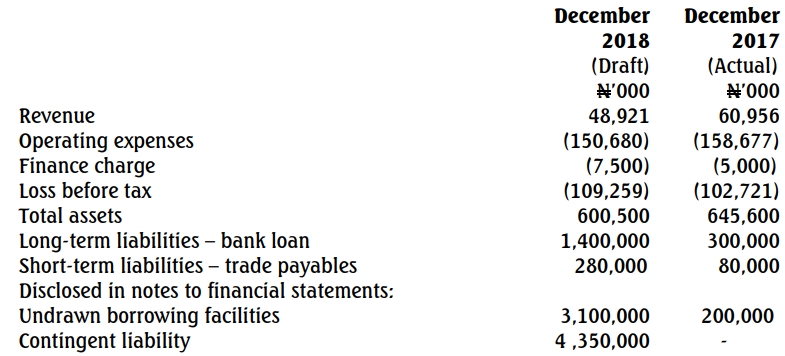

- 15 Marks

AAA – May 2016 – L3 – Q6 – Audit Reporting

Discuss audit work and written representation letter for legal claims, outstanding balances, and investments.

Question

Bob Removals Limited is a removals company. In the year ended December 31, 2015, the company made a trading profit of N800,000. You are the manager in charge of the audit.

The following issues have arisen:

(i) A customer is suing the company for N1 million for damage caused to antique furniture. The company is defending the claim and believes that the furniture was a reproduction as opposed to antique and therefore worth only N100,000.

(ii) A balance due from Safe Storage in respect of sub-contract work, of N300,000, has been outstanding for over six months. Your firm has been asked by Bob Removals’ accountant not to write to Safe Storage for direct confirmation of this amount as the latter company objects to such letters. You have been assured by the accountant that the relationship between the two companies is good and that the outstanding balance will be paid.

(iii) Bob Removals has recently invested in four new removal vans and is currently carrying out extensive refurbishment of its premises. As a result of this expenditure, the company has reached its overdraft limit of N500,000.

Required:

For each of the above issues:

a. State, with reasons, the audit work that you would expect to find when undertaking your review of the audit working papers for the year ended December 31, 2015.

b. Draft the relevant sections dealing with these issues of the written representation letter you would wish the directors to sign.

Find Related Questions by Tags, levels, etc.

- Tags: Audit Procedures, Investment, Legal Claim, Outstanding Balance, Written Representation

- Level: Level 3

- Topic: Audit Reporting