- 5 Marks

MA – Nov 2024 – L2 – Q4b – Standard Costing and Variance Investigation

Explanation of the use of standard costing in decision-making and key factors to consider before investigating variances.

Question

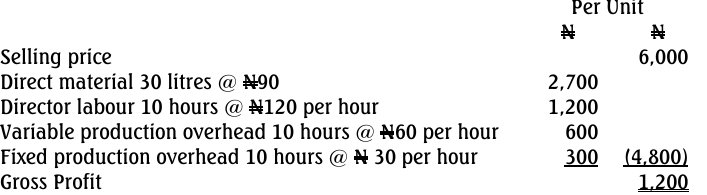

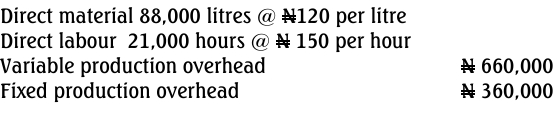

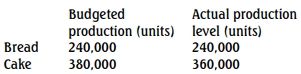

Standard costing has been employed by organizations as a control technique to analyze the deviation of results from those that are expected.

Required:

i) Explain TWO ways managers have effectively deployed standard costing as a tool in decision-making analysis.

ii) Explain THREE key factors a manager should consider before deciding to institute an investigation into reported variances.

Find Related Questions by Tags, levels, etc.

- Tags: Cost Control, Performance Evaluation, Standard Costing, Variance Analysis

- Level: Level 2

- Topic: Standard Costing and Variance Analysis

- Series: Nov 2024