Question

The following figures have been extracted from the accounting records of Skolom Ltd on 31 December 2022:

Additional information provided includes notes on Skolom Ltd’s agency arrangements with Keke Ltd, joint venture details, and depreciation policies.

Required:

Prepare for Skolom Ltd in accordance with International Financial Reporting Standards (IFRSs):

a) Statement of Comprehensive Income for the year ended 31 December 2022

b) Statement of Financial Position as at 31 December 2022

Answer

Question

The following is the trial balance of Kwadaso Ltd, a trading company, as at 30 September 2015:

Additional Information:

- On 31 March 2015, the company made a bonus issue from retained earnings of one new share for every four shares in issue at GH¢10.00 each. This transaction is yet to be recorded in the books. The company paid ordinary dividends of GH¢2.2 per share on 31 January 2015 and GH¢2.6 per share on 30 June 2015. The dividend payments are included in administrative expenses in the trial balance.

- Provision is to be made for a full year’s interest on the Loan notes.

- The finance charge relating to the preference shares is equal to the dividend payable.

- Non-current assets:

- Depreciation of Property, Plant, and Equipment is to be provided on the following bases:

- Plant and equipment – 10% on cost

- Computer equipment – 25% on cost

- Motor vehicles – 20% on reducing balance

- No depreciation has yet been charged on any non-current asset for the year ended 30 September 2015.

- Kwadaso revalues its buildings at the end of each accounting year. At 30 September 2015, the relevant value to be incorporated into the financial statements is GH¢14,100,000. The building’s remaining life at the beginning of the current year (1 October 2014) was 25 years. Kwadaso does not make an annual transfer from the revaluation reserve to retained earnings in respect of the realisation of the revaluation surplus. Ignore deferred tax on the revaluation surplus.

- Depreciation of Property, Plant, and Equipment is to be provided on the following bases:

- The available-for-sale investments held at 30 September 2015 had a fair value of GH¢8,400,000. There were no acquisitions or disposals of these investments during the year.

- In February 2015, Kwadaso’s internal audit unit discovered a fraud committed by the company’s credit manager who did not return from a foreign business trip. The outcome of the fraud is that GH¢500,000 of the company’s trade receivables have been stolen by the credit manager and are not recoverable. Of this amount, GH¢200,000 relates to the year ended 30 September 2014 and the remainder to the current year. Kwadaso is not insured against this fraud.

- Corporate income tax payable estimated on the profit for the year is GH¢3,500,000. An amount of GH¢1,200,000 is to be transferred to the deferred taxation account.

Required:

Prepare the following financial statements of Kwadaso Ltd for publication in accordance with International Financial Reporting Standards (IFRS):

a) Statement of profit or loss and other comprehensive income for the year ended 30 September 2015.

b) Statement of changes in equity for the year ended 30 September 2015.

c) Statement of financial position as at 30 September 2015.

d) Show clearly all relevant workings.

(Note: Accounting policy notes are not required)

Answer

Question

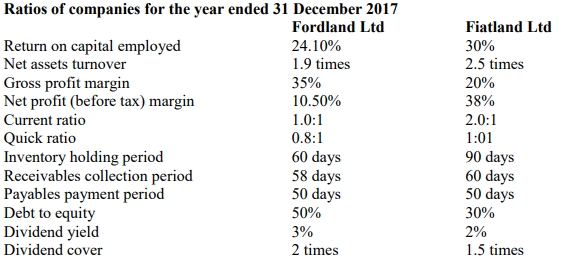

Fordland Ltd and Fiatland Ltd are two companies in the garment industry. The following are financial ratios computed by the Research Department of ICAG as part of analyzing companies’ performance industry by industry.

Required:

Explain THREE problems that are inherent when ratios are used to compare the performance of two companies, even in the same industry.

Answer

Question

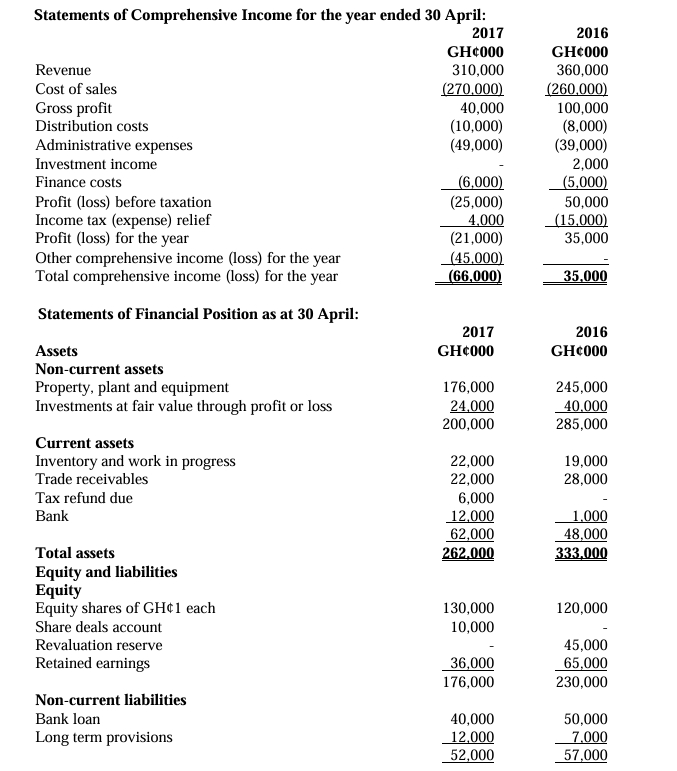

Ahomka Ltd is a public listed manufacturing company. Its summarised financial statements for the year ended 30 April 2017 (and 2016 comparatives) are as follows:

The following additional information is available:

i) There were no additions to, or disposals of, non-current assets during the year.

ii) In order to help cash flows, the company made a rights issue of shares during the year ending 30 April 2017, all of which ranked for dividend. No shares were issued during the year ended 30 April 2016.

iii) The dividend per share has been reduced by 50% for the year ended 30 April 2017.

Required:

a) Prepare a statement of changes in equity for years ended 30 April 2016 and 2017 for Ahomka Ltd as the above information permits.

b) Analyze and discuss the financial performance and financial position of Ahomka Ltd as portrayed in the financial statements and in the additional information provided. Your analysis should be supported by relevant ratios.

Answer

Question

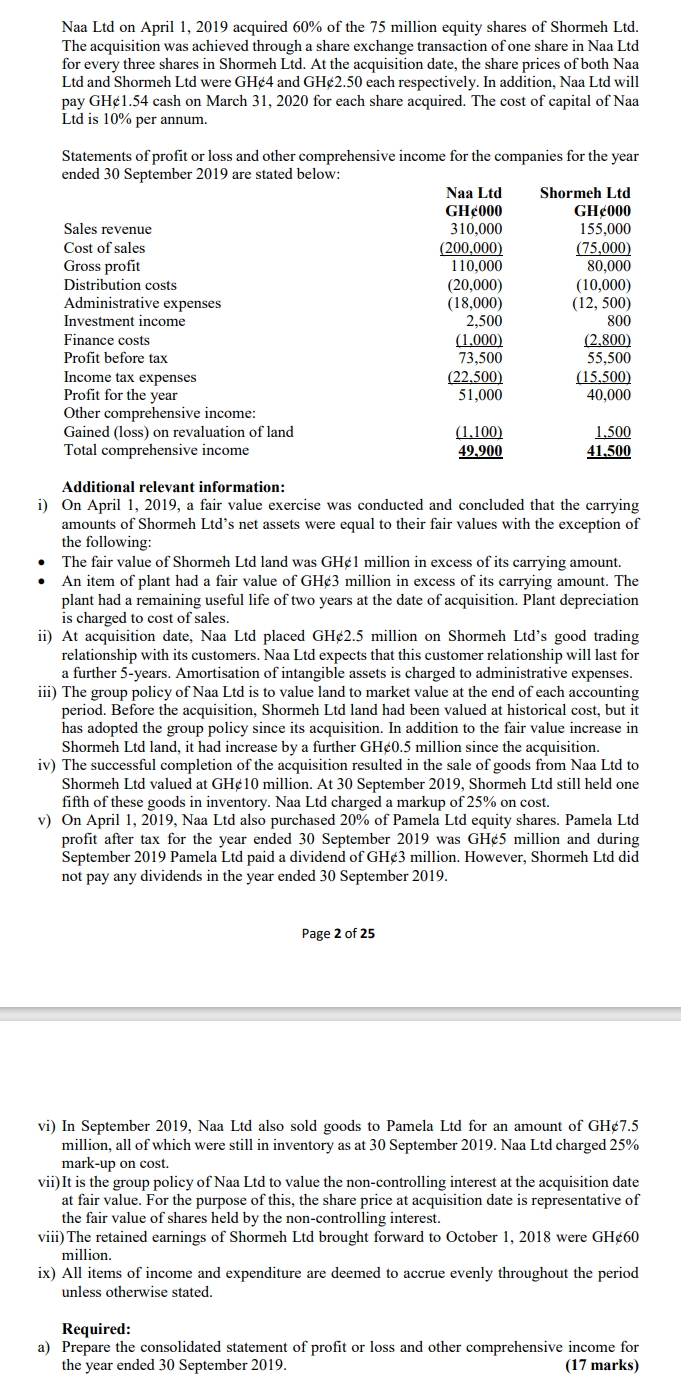

The following figures have been extracted from the accounting records of Skolom Ltd on 31 December 2022:

Additional information provided includes notes on Skolom Ltd’s agency arrangements with Keke Ltd, joint venture details, and depreciation policies.

Required:

Prepare for Skolom Ltd in accordance with International Financial Reporting Standards (IFRSs):

a) Statement of Comprehensive Income for the year ended 31 December 2022

b) Statement of Financial Position as at 31 December 2022

Answer

Question

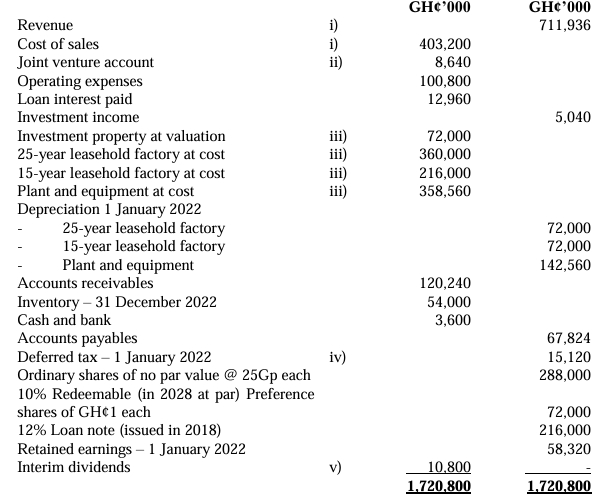

The following is the trial balance of Kwadaso Ltd, a trading company, as at 30 September 2015:

Additional Information:

- On 31 March 2015, the company made a bonus issue from retained earnings of one new share for every four shares in issue at GH¢10.00 each. This transaction is yet to be recorded in the books. The company paid ordinary dividends of GH¢2.2 per share on 31 January 2015 and GH¢2.6 per share on 30 June 2015. The dividend payments are included in administrative expenses in the trial balance.

- Provision is to be made for a full year’s interest on the Loan notes.

- The finance charge relating to the preference shares is equal to the dividend payable.

- Non-current assets:

- Depreciation of Property, Plant, and Equipment is to be provided on the following bases:

- Plant and equipment – 10% on cost

- Computer equipment – 25% on cost

- Motor vehicles – 20% on reducing balance

- No depreciation has yet been charged on any non-current asset for the year ended 30 September 2015.

- Kwadaso revalues its buildings at the end of each accounting year. At 30 September 2015, the relevant value to be incorporated into the financial statements is GH¢14,100,000. The building’s remaining life at the beginning of the current year (1 October 2014) was 25 years. Kwadaso does not make an annual transfer from the revaluation reserve to retained earnings in respect of the realisation of the revaluation surplus. Ignore deferred tax on the revaluation surplus.

- Depreciation of Property, Plant, and Equipment is to be provided on the following bases:

- The available-for-sale investments held at 30 September 2015 had a fair value of GH¢8,400,000. There were no acquisitions or disposals of these investments during the year.

- In February 2015, Kwadaso’s internal audit unit discovered a fraud committed by the company’s credit manager who did not return from a foreign business trip. The outcome of the fraud is that GH¢500,000 of the company’s trade receivables have been stolen by the credit manager and are not recoverable. Of this amount, GH¢200,000 relates to the year ended 30 September 2014 and the remainder to the current year. Kwadaso is not insured against this fraud.

- Corporate income tax payable estimated on the profit for the year is GH¢3,500,000. An amount of GH¢1,200,000 is to be transferred to the deferred taxation account.

Required:

Prepare the following financial statements of Kwadaso Ltd for publication in accordance with International Financial Reporting Standards (IFRS):

a) Statement of profit or loss and other comprehensive income for the year ended 30 September 2015.

b) Statement of changes in equity for the year ended 30 September 2015.

c) Statement of financial position as at 30 September 2015.

d) Show clearly all relevant workings.

(Note: Accounting policy notes are not required)

Answer

Question

Fordland Ltd and Fiatland Ltd are two companies in the garment industry. The following are financial ratios computed by the Research Department of ICAG as part of analyzing companies’ performance industry by industry.

Required:

Explain THREE problems that are inherent when ratios are used to compare the performance of two companies, even in the same industry.

Answer

Question

Ahomka Ltd is a public listed manufacturing company. Its summarised financial statements for the year ended 30 April 2017 (and 2016 comparatives) are as follows:

The following additional information is available:

i) There were no additions to, or disposals of, non-current assets during the year.

ii) In order to help cash flows, the company made a rights issue of shares during the year ending 30 April 2017, all of which ranked for dividend. No shares were issued during the year ended 30 April 2016.

iii) The dividend per share has been reduced by 50% for the year ended 30 April 2017.

Required:

a) Prepare a statement of changes in equity for years ended 30 April 2016 and 2017 for Ahomka Ltd as the above information permits.

b) Analyze and discuss the financial performance and financial position of Ahomka Ltd as portrayed in the financial statements and in the additional information provided. Your analysis should be supported by relevant ratios.