Question

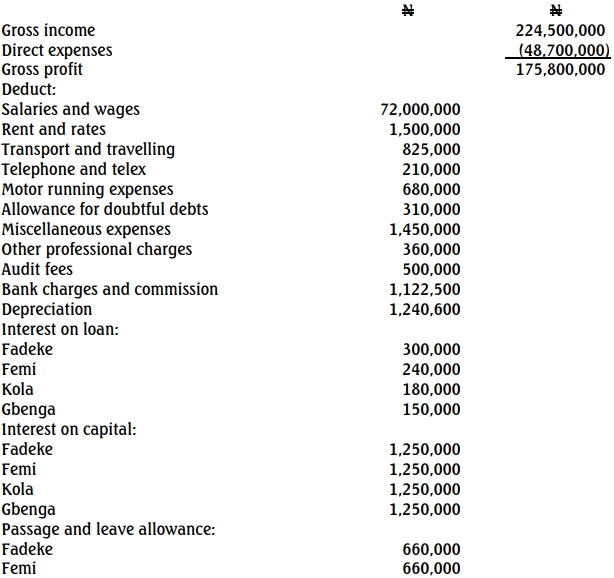

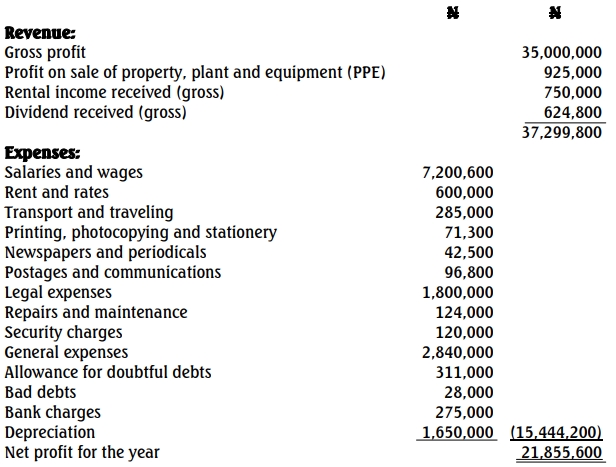

Alhaji Nura Imam, having spent over 20 years as an employee of Apex Limited, retired on November 1, 2020. On January 2, 2021, he registered a business under the name of Nura Imam Enterprises. The profit or loss account of the enterprise for the year ended December 31, 2021, is as follows:

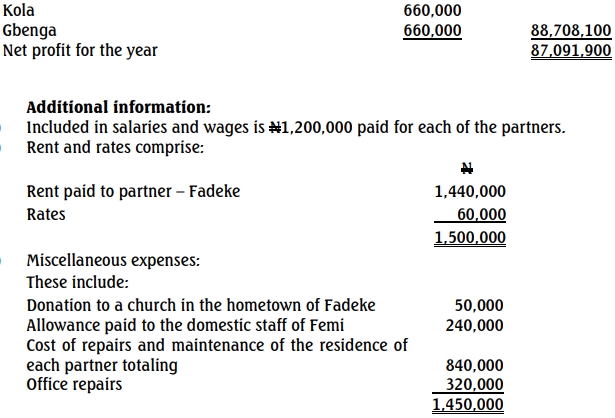

You were provided with the following additional information:

(v) Agreed capital allowance on qualifying capital expenditure was N1,240,000.

(vi) Alhaji Imam received a gratuity of N4,000,000 during the year.

(vii) Alhaji Imam is blessed with five children, all within the ranges of 10 to 21 years.

(viii) The proprietor has a life assurance policy on which he pays a premium of N1,200,000 annually.

Required: Compute the personal income tax payable by Alhaji Nura Imam for the relevant assessment year. (30 Marks)