- 16 Marks

MA – Nov 2024 – L2 – Q5a – Limiting Factor Decision and Profit Maximization

Determination of the optimum production plan considering scarce resources.

Question

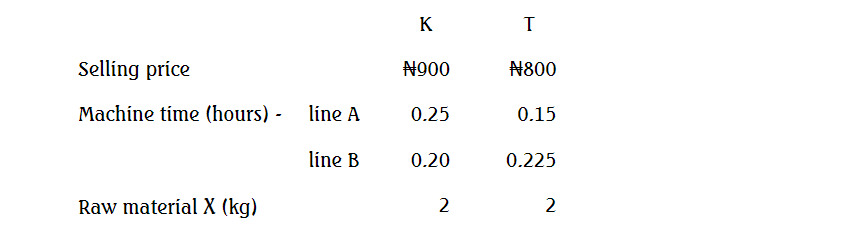

Manche produces two products from different quantities of the same resources using a just-in-time (JIT) production system. The selling price and resource requirements of each of the products are shown below:

| Product | C | L |

|---|---|---|

| Unit Selling Price (GH¢) | 130 | 160 |

| Resources per Unit: | ||

| Direct Labour (GH¢8 per hour) | 3 hours | 5 hours |

| Material A (GH¢3 per kg) | 5 kg | 4 kg |

| Material B (GH¢7 per litre) | 2 litres | 1 litre |

| Machine Hours (GH¢10 per hour) | 3 hours | 4 hours |

| Fixed Overhead (GH¢8 per hour) | 1 hour | 1 hour |

Market research shows that the maximum demand for products C and L during August 2024 is 500 units and 800 units respectively. This does not include an order that Manche has agreed with a commercial customer for the supply of 250 units of C and 350 units of L at selling prices of GH¢100 and GH¢135 per unit, respectively. Failure by Manche to deliver the order in full by the end of August will cause Manche to incur a GH¢5,000 financial penalty.

At a recent meeting between the Purchasing Manager and Production Manager to discuss the production plans of C and L for August, the following resource restrictions for the year were identified:

- Direct Labour Hours: 90,000 hours

- Machine Hours: 90,000 hours

The resource restrictions were evenly distributed throughout the year.

Required:

i) Prepare the optimum production plan for August 2024 using relevant computations.

ii) Determine the contribution from adopting this plan.

iii) Using relevant computations, show whether Manche should complete the order from the commercial customer assuming any excess labour hours for not making the contract can be used to produce 300 units of product ‘F’ with a contribution of GH¢55 per unit.

Find Related Questions by Tags, levels, etc.

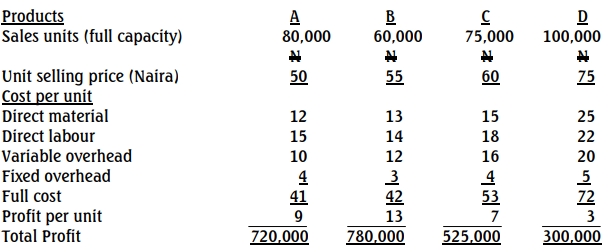

The following data relates to the planned activity of three products of Parlour Plc:

The following data relates to the planned activity of three products of Parlour Plc: