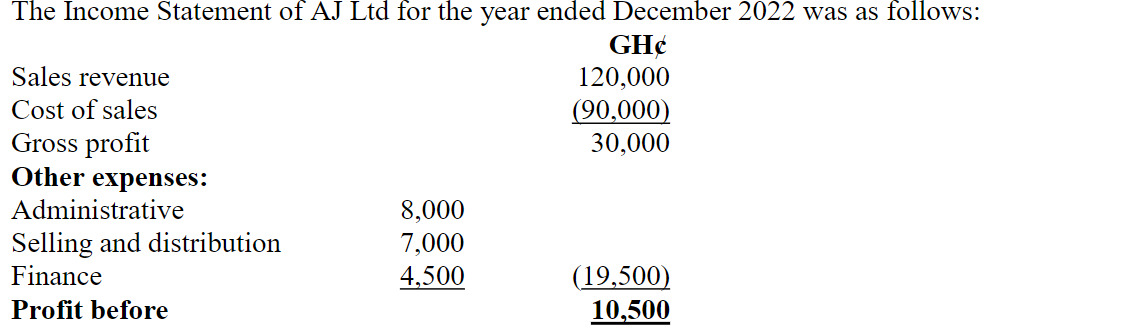

- 15 Marks

MA – Nov 2024 – L2 – Q2a – Budgetary Control

Preparation of a budgeted profit and loss account for Ankawa LTD for the year ending 31 December 2025.

Question

Ankawa LTD makes and sells a single product ‘Dee’. The following information is available for use in the budgeting process for the year 2025.

i) Sales targets have been proposed for four quarters in 2025 and the first quarter in 2026:

| Year | Quarter 1 | Quarter 2 | Quarter 3 | Quarter 4 | Quarter 1 (2026) |

|---|---|---|---|---|---|

| Sales (GH¢) | 240,000 | 160,000 | 144,000 | 224,000 | 192,000 |

Selling price per unit of Dee is expected to be GH¢20.

ii) Inventory levels

-

At 31 December 2024: Finished units of Dee: 3,000 units

-

Raw materials: 7,000kg

-

Closing inventory of finished product Dee at the end of each quarter is budgeted as a percentage of sales units of the following quarter:

- Quarters 1 and 2: 25%

- Quarters 3 and 4: 35%

-

Closing inventory of raw materials is budgeted to fall by 600kg at the end of each quarter.

iii) Product Dee unit data:

- Material: 8kg at GH¢1.60 per kg

- Direct labour: 1.2 hours at GH¢3.50 per hour

iv) Other budgeted quarterly expenditure for 2025:

| Quarter | Fixed Overhead (GH¢) | Capital Expenditure (GH¢) |

|---|---|---|

| Quarter 1 | 10,000 | 10,000 |

| Quarter 2 | 18,000 | – |

| Quarter 3 | 27,000 | – |

| Quarter 4 | 30,000 | – |

v) Depreciation

- Property is depreciated on a straight-line basis at 5% per annum based on total cost.

- Value of property as at 31 December 2024: GH¢100,000.

vi) Inventory of product Dee is valued on a marginal cost basis for internal budget purposes.

Required:

Prepare the budgeted profit and loss account for the year ended 31 December 2025.

Find Related Questions by Tags, levels, etc.

- Tags: Budgeting, Costing, Financial planning, Forecasting, Profit and Loss

- Level: Level 2

- Topic: Budgetary control

- Series: Nov 2024