Question

Answer

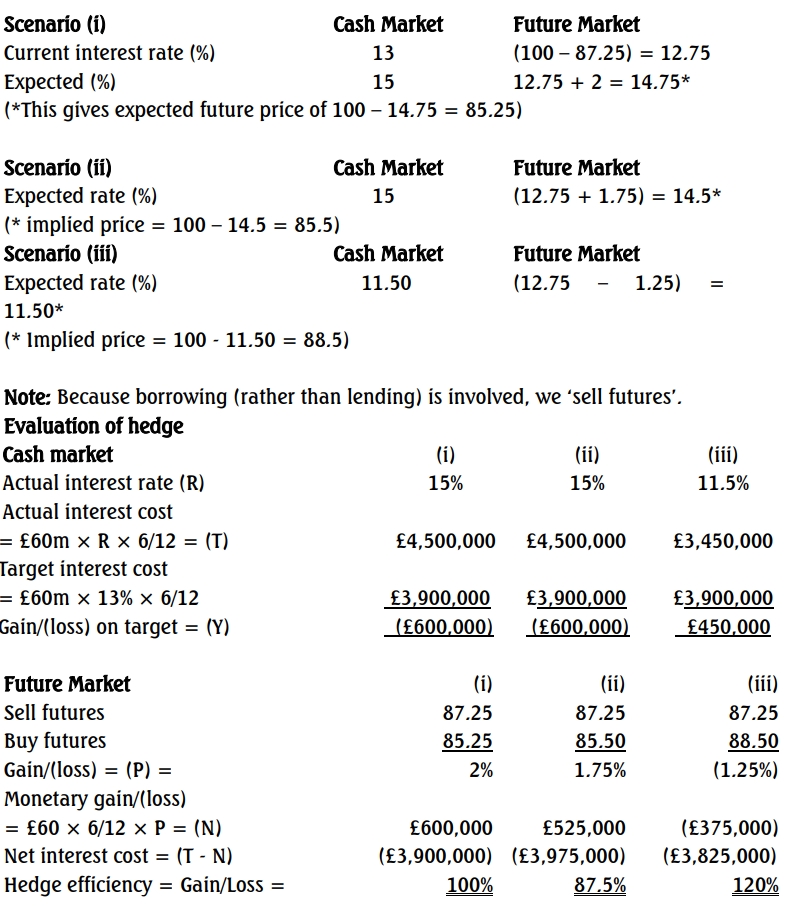

a) Note:

For each of the scenarios of interest rate movements given in the question, we need to identify the appropriate market price of the futures contracts. Generally, the movements in interest rates and futures prices should be in the same direction but not necessarily „one-on-one‟.

b) Interest rate guarantee (IRG)

Premium for the guarantee is: £60m × 0.25% = £150,000.

The guarantee would be used in cases (i) and (ii) because the actual rate (15%) is greater than the target rate (13%).

Then, total cost limiting interest rates to 13% is actual interest of £3,900,000 plus premium £150,000, that is, £4,050,000. This costs more than the futures contracts hedge in cases (i) and (ii). In case

(iii), the guarantee is not used because the prevailing interest rate of 11.5% is less than the guarantee rate of 13%.

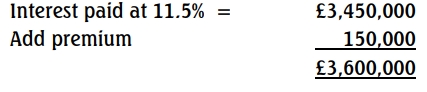

Interest costs at 11.5% are:

This costs less than the futures hedge, reflecting the fact that declining to take up the interest rate option in the case of the guarantee, has allowed the company to take advantage of the lower interest rates in the cash market.