Question

Answer

ONDO TELECOMS LIMITED

Financial Statements (Under IFRS) for the Year Ended 30 September 2014

i. Non-Current Assets Held for Sale (or Disposal)

Application of IFRS 5:

The provision of IFRS 5 should be applied for this transaction. According to the standard, the following conditions must be met for an asset to be classified as held for sale:

a. The asset must be available for immediate sale in its present condition, subject only to terms that are usual and customary for the sale of such assets. This is evidenced by management seeking buyers as shown by the bids.

b. The sale must be highly probable.

c. The sale is to be completed within a year from the date of classification.

Since Ondo Telecoms has negotiated with four serious bidders and expects the sale to be concluded by May 2015, these conditions are satisfied.

Measurement:

The asset should be measured at the lower of its carrying amount and fair value less costs to sell.

Computation:

- Carrying Amount (as at 30 September 2013): N4.5 billion.

- Fair Value Less Costs to Sell:

- Fair value: N4.2 billion.

- Less transaction costs: N0.3 million.

- Resulting value: N4.1997 billion.

The lower value, N4.1997 billion, will serve as the carrying amount as at 30 September 2014.

The difference between the carrying amount (N4.5 billion) and the fair value less costs to sell (N4.1997 billion) will be expensed during the year ended 30 September 2014.

Discontinued Operations:

- A discontinued operation is a component of an entity that has either been disposed of or classified as held for sale.

- Since this transaction involves a whole segment classified as held for sale, it should be presented as discontinued operations with the following disclosures:

- Loss for the Year (2014): N1.7 billion, shown separately in the Statement of Comprehensive Income.

- Prior Year Loss (2013): N0.8 billion, restated for comparative purposes.

ii. Block of Flats – Accounting Treatment

Applicable Standards:

The block of flats should be accounted for as Property, Plant, and Equipment (PPE) under IAS 16.

The property does not qualify as an investment property under IAS 40 because it is occupied by staff, even if they are paying market rates.

Recognition and Disclosure Principles:

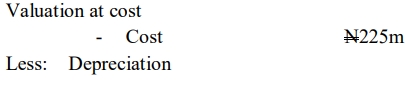

- The block of flats could be carried:

- At cost less depreciation:

- Depreciation is charged systematically over its useful life, estimated at 50 years.

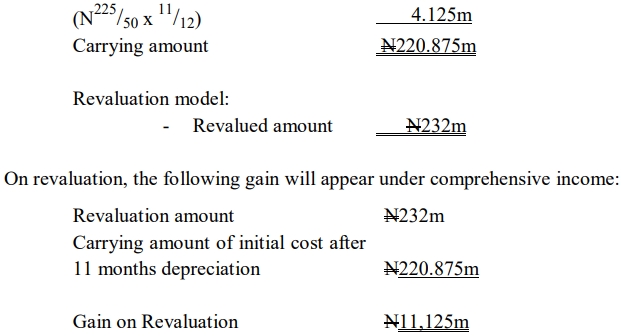

- At revaluation model/basis:

- The property is periodically revalued, and gains or losses arising from revaluation are recognized in other comprehensive income.

- At cost less depreciation:

iii. Valuation of Customer Balances (Lists)

Treatment under IAS 38:

Ondo Telecoms Limited’s customer list of balances is an internally generated intangible asset. However, it does not qualify for recognition under IAS 38 because the internal costs of producing these items cannot be separately distinguished from the costs of delivering and operating the business as a whole.

Recognition Criteria:

- If the customer list had been purchased separately, as in the case of International Telecom Limited’s acquisition of Edo Communications Limited, it would qualify for recognition as an intangible asset.

- However, since the customer list was internally generated, it fails the recognition test.

Key Consideration:

While the CFO of Ondo Telecoms Limited expects to derive future economic benefits from these customers, the entity cannot recognize the value of the customer list in its financial statements because:

- Lack of Control: The entity does not have control over the loyalty or retention of the customers.

- Internally Generated Asset: The customer list remains an internally generated intangible asset unless it is packaged and sold separately to a buyer.

iv. Impairment of Television License

Impairment under IAS 36:

At the end of the first year after acquisition, the market value of the television license has declined to N420 million as at 30 September 2014, due to the slow uptake of the television business.

Fair Value as Recoverable Amount:

- If the fair value of N420 million represents the recoverable amount, this indicates that the license has suffered impairment.

- An impairment loss should be recognized in accordance with IAS 36.

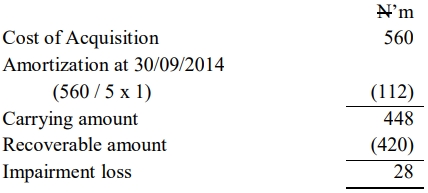

Computation of Impairment:

- Carrying Amount: N560 million (initial recognition).

- Recoverable Amount: N420 million (fair value).

- Impairment Loss: Impairment Loss=Carrying Amount−Recoverable Amount=560 million−420 million=140 million.

Accounting Treatment:

The impairment loss of N140 million should be charged to the income statement for the year ended 30 September 2014.

The computation is as follows: