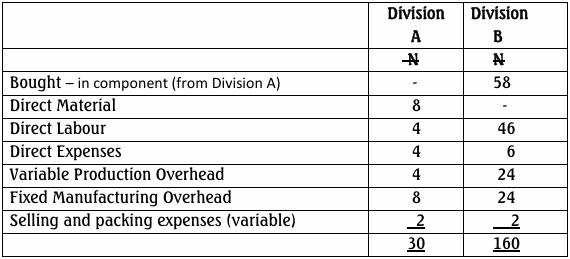

- 10 Marks

MA – Nov 2024 – L2- Q1b – Return on Investment (ROI)

Computation of ROI for different one-off transactions and advice on whether they should be undertaken.

Question

Dondo LTD is a manufacturing company based in Nsawam. The following data represents the budgeted performance of Dondo LTD for the year 2025:

| Amount (GH¢’000) | |

|---|---|

| Profit | 660 |

| Plant and equipment (net of depreciation) | 1,560 |

| Working capital | 750 |

Dondo LTD is considering undertaking the following separate one-off transactions:

- A cash discount of GH¢16,000 will be offered to its customers annually. This will, on average, reduce the trade receivables figure by GH¢60,000.

- An increase in average inventories by GH¢80,000 throughout the year. The increased inventory level is expected to increase sales, resulting in GH¢30,000 increased contribution per annum.

- At the beginning of the year, the company will buy a plant worth GH¢360,000. This is expected to reduce operating costs by GH¢105,000. The plant has a five-year useful life with nil residual value.

Required:

i) Compute the ROI for each of the one-off transactions above.

ii) Advise Dondo LTD on whether the above one-off transactions should be carried out.

Find Related Questions by Tags, levels, etc.

- Tags: Cost Control, Decision Making, Financial Performance, Investment Appraisal, ROI

- Level: Level 2

- Topic: Performance analysis

- Series: Nov 2024