Question

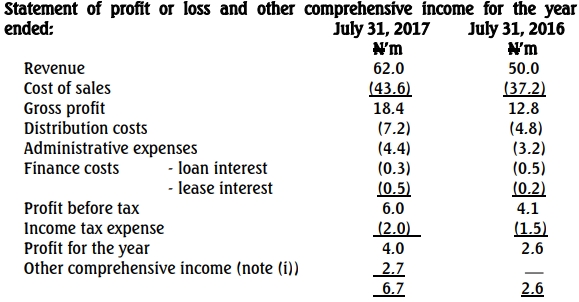

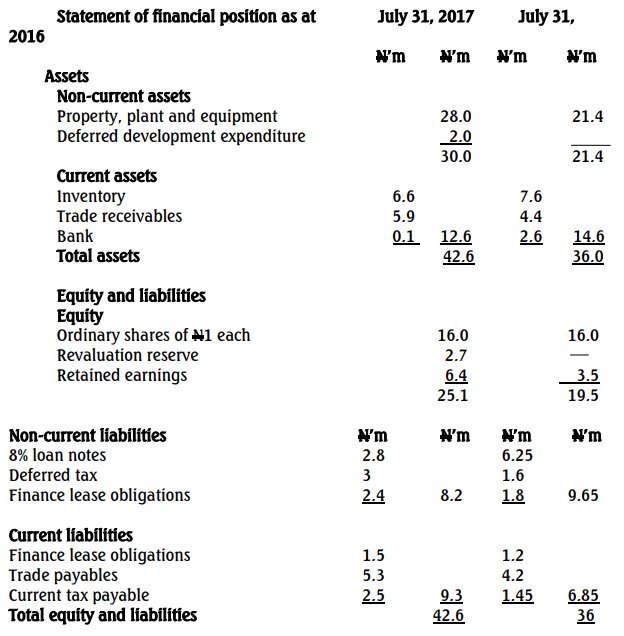

Happy is a publicly listed company. Its financial statements for the year ended July 31, 2017, including comparatives, are shown below:

Notes:

- On November 1, 2016, Happy acquired an additional plant under a finance lease with a fair value of ₦3 million. The property was also revalued upward by ₦4 million, with ₦1.3 million of the revaluation reserve transferred to deferred tax. No disposals occurred during the period.

- Depreciation on property, plant, and equipment amounted to ₦1.8 million, and amortization of deferred development expenditure was ₦0.4 million.

Required:

Prepare the statement of cash flows of Happy Plc for the year ended July 31, 2017, in accordance with IAS 7, using the indirect method. (20 Marks)