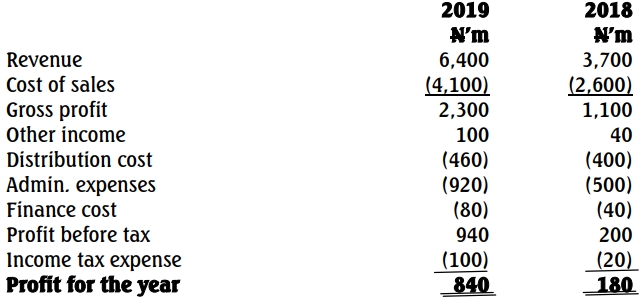

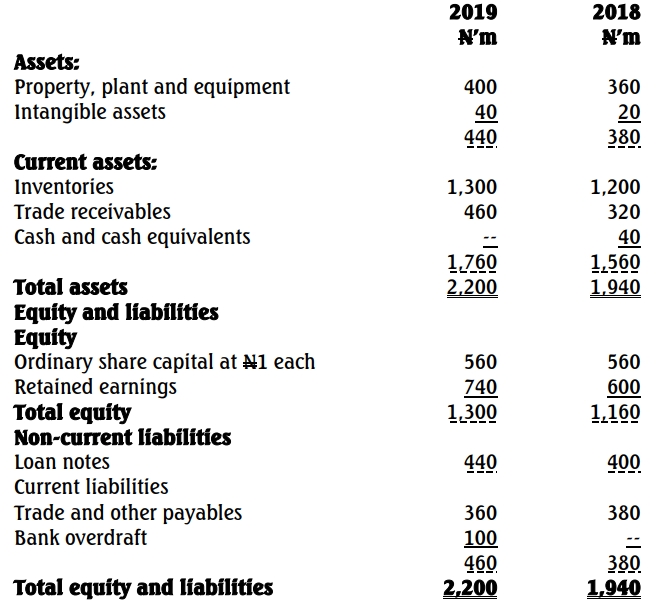

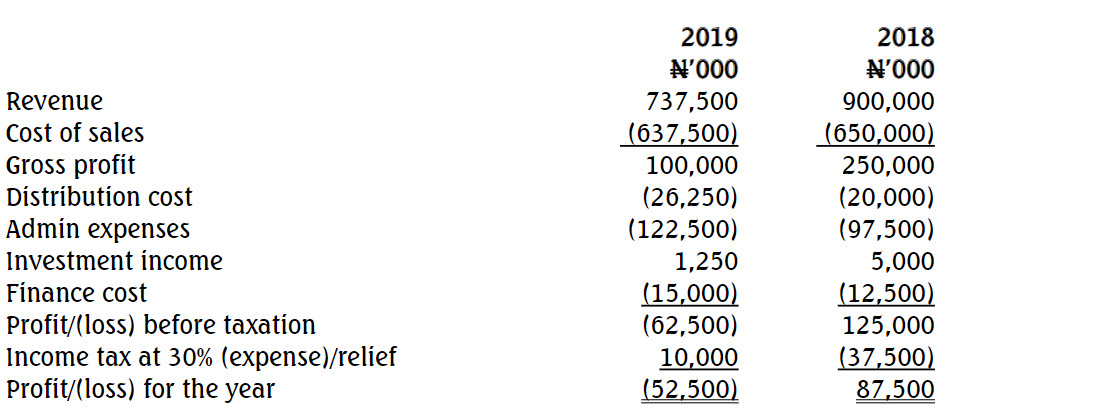

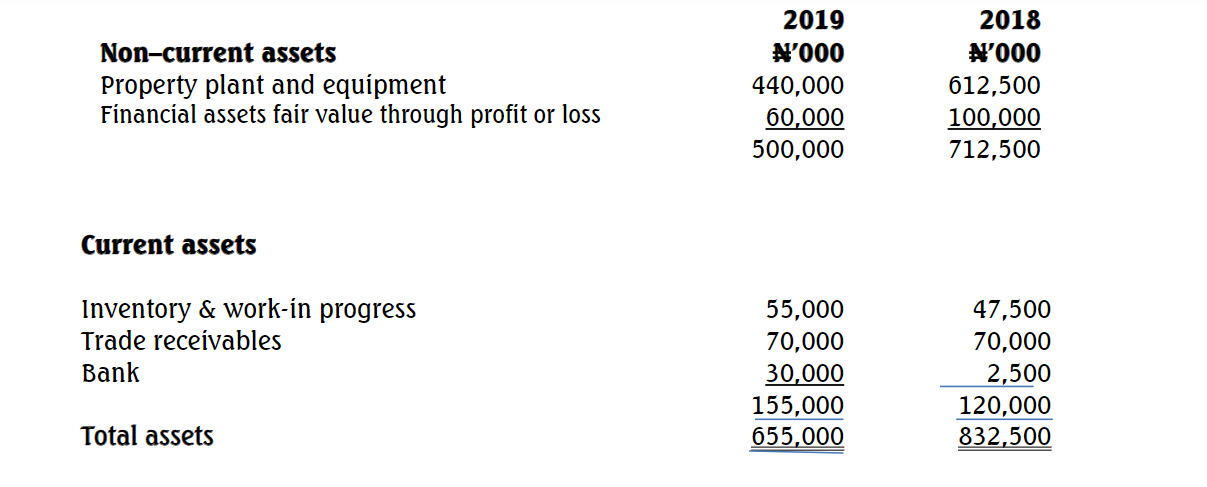

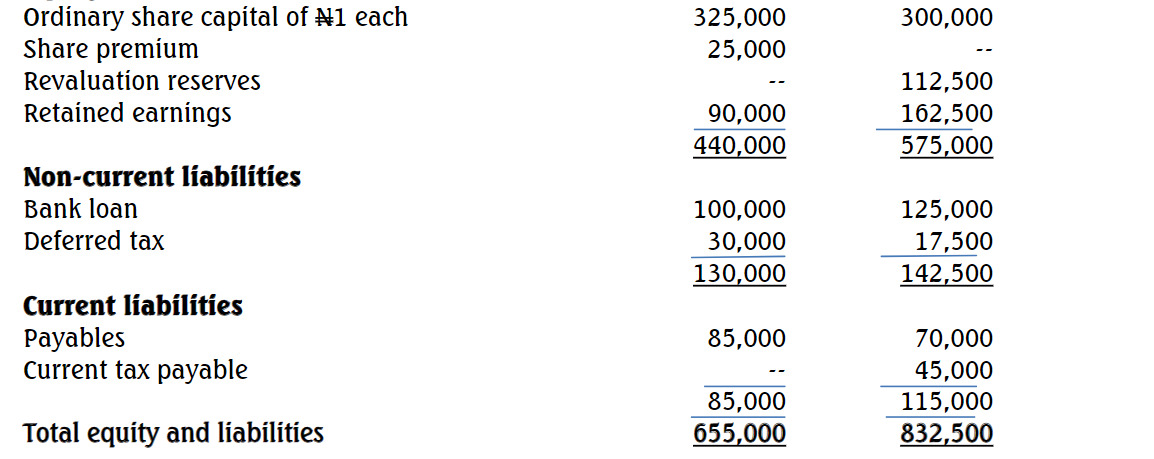

Dangoyaro Plc is a manufacturing company, and the summarized financial statements for the year ended September 30, 2019, and the comparative figures for 2018 are as follows:

Statement of Financial Position as at September 30

Equity and liabilities

Equity

The following information was obtained from the chairman’s statement in the annual report presented at the Annual General Meeting (AGM) held on December 22, 2019, and in the notes to the financial statements.

(i) Market condition during the year ended September 30, 2019, proved very challenging due largely to difficulties in the global economy as a result of the recession, which led to a decline in the share price and property values.

(ii) Dangoyaro Plc has not been immune from these effects and our properties have suffered impairment losses of ₦125 million in the year. The excess of these losses over previous surpluses has led to a charge to cost of sales of ₦37.5 million in addition to the normal depreciation charge.

(iii) There is no addition to or disposal of non-current assets during the year.

(iv) In response to the downturn, the company has made a number of employees redundant, incurring severance costs of ₦32.5 million (included in cost of sales), undertaken cost savings in advertising and other administrative expenses.

(v) The difficulty in the credit market has meant that the finance cost of our fixed interest bank loan has increased from ₦12.5 million to ₦15 million. In order to improve cash flows, the company made a rights issue during the year and reduced the dividend per share by 50%.

(vi) Despite the above events and the associated costs, the board of directors of Dangoyaro Plc believes the company’s performance has been quite resilient in these difficult times.

You are required to prepare:

a. An adjusted statement of profit or loss for the year ended September 30, 2019 (without taking into consideration information in the chairman’s statement and notes to the financial statements). (5 Marks)

b. Statement of changes in equity for the year ended September 30, 2019. (8 Marks)

c. Statement of cash flows for the year ended September 30, 2019, using the indirect method in accordance with provisions of IAS 7. (12 Marks)

d. Analyse and discuss the financial performance and position of Dangoyaro Plc as shown by the above financial statements as at September 30, 2019, using the following financial ratios:

i. Gross profit margin

ii. Net profit margin

iii. Return on capital employed (CE = ordinary shares plus reserves)

iv. Asset turnover

v. Current ratio

vi. Quick ratio

vii. Gearing ratio

viii. Receivables period

ix. Inventory period

x. Payables period

(15 Marks)

(Total 40 Marks)