Question

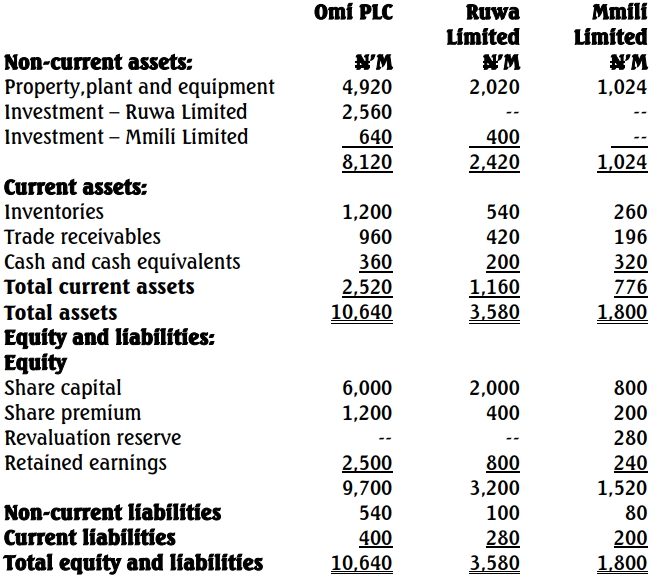

The draft statement of financial position of Omi PLC, Ruwa Limited, and Mmili Limited as of November 30, 2020, are as follows:

Additional Information for Consolidated Financial Statements Preparation:

- Acquisition of Ruwa Limited:

- Omi PLC acquired 80% of Ruwa Limited’s ordinary share capital on December 1, 2017.

- Retained earnings of Ruwa Limited at acquisition: N400 million.

- Fair value of Ruwa Limited’s net assets: N2,840 million.

- Any fair value adjustment pertains to net current assets, which had been realized by November 30, 2020.

- No new issue of shares occurred in the group since the establishment of the current structure.

- Acquisition of Mmili Limited:

- On December 1, 2018, Omi PLC acquired 40% and Ruwa Limited acquired 25% of Mmili Limited’s ordinary share capital.

- Retained earnings of Mmili Limited at acquisition: N200 million.

- Retained earnings of Ruwa Limited at acquisition: N600 million.

- No revaluation surplus existed in Mmili Limited’s books at acquisition, and the fair value of Mmili Limited’s net assets was consistent with their carrying amount.

- Development Costs:

- Significant expenditure incurred on developing internet products. These were initially written off but later reinstated as development inventories upon commercial use.

- Costs do not meet the recognition criteria of IAS 38 – Intangible Assets.

- Ruwa Limited included N80 million of these costs in its inventory, of which N20 million relates to expenses from periods before December 1, 2017.

- The group wishes to ensure compliance with IFRS for this treatment.

- Internet Equipment:

- Ruwa Limited purchased new internet equipment for N200 million, excluding a trade discount of N24 million.

- The discount was recorded in the income statement.

- Depreciation is calculated using the straight-line method over six years.

- Property, Plant, and Equipment Policy:

- The group transitioned from the revaluation model to the cost model under IAS 16 – Property, Plant, and Equipment in 2020.

- Mmili Limited’s assets were revalued on December 1, 2019, creating a revaluation surplus of N280 million.

- Mmili Limited’s property was originally purchased in December 2018 for N1,200 million, with depreciation over six years.

- The group does not transfer excess depreciation from revaluation reserves to retained earnings.

- Valuation of Non-controlling Interests:

- The group values non-controlling interests at acquisition using their proportionate share of the subsidiary’s identifiable net assets.

- Defined Benefit Pension Scheme:

- Omi PLC established a defined benefit pension scheme, contributing N400 million to it.

- Details as of November 30, 2020:

- Present value of obligation: N520 million.

- Fair value of plan assets: N500 million.

- Current service cost: N440 million.

- Interest cost (scheme liabilities): N80 million.

- Expected return on pension assets: N40 million.

- Actuarial gain: N60 million.

- The only recorded entry was the cash contribution, included in Omi PLC’s trade receivables.

- Directors propose recognizing actuarial gain immediately in the statement of profit or loss.

Required:

Prepare the consolidated statement of financial position of Omi Group for the year ended November 30, 2020, in accordance with relevant IFRS.