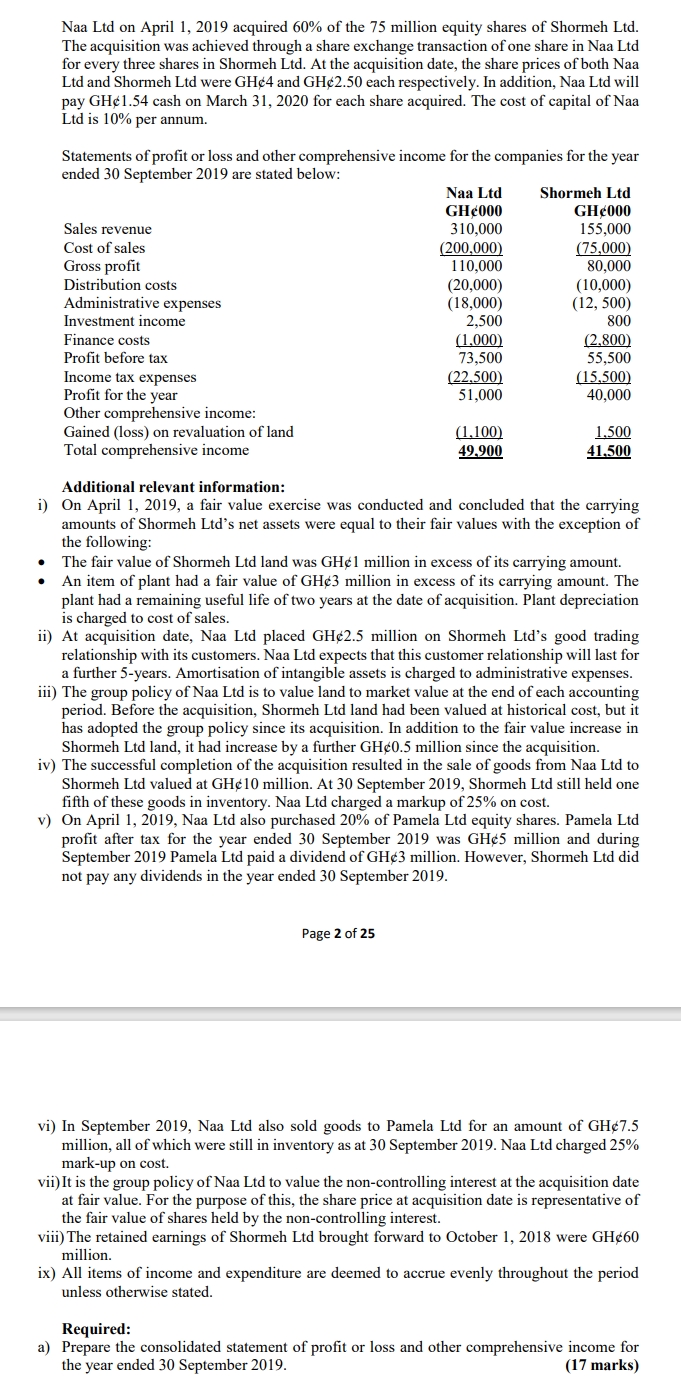

Komolafe Group carries on business as a distributor of warehouse equipment and importer of fruit into the country. Komolafe was incorporated in 2008 to distribute warehouse equipment. It diversified its activities during the year 2010 to include the import and distribution of fruit, and expanded its operations by the acquisition of shares in Kelvins in 2012 and Kelly in 2014.

Accounts for all companies are made up to December 31.

The draft statements of profit or loss and other comprehensive income for Komolafe, Kelvins, and Kelly for the year ended December 31, 2016 are as follows:

|

Komolafe |

Kelvins |

Kelly |

| Revenue |

91,200 |

49,400 |

45,600 |

| Cost of sales |

(36,100) |

(10,926) |

(10,640) |

| Gross profit |

55,100 |

38,474 |

34,960 |

| Distribution costs |

(6,650) |

(4,274) |

(3,800) |

| Administrative expenses |

(6,950) |

(1,900) |

(3,800) |

| Finance costs |

(650) |

– |

– |

| Profit before tax |

40,850 |

32,300 |

27,360 |

| Income tax expense |

(16,600) |

(10,780) |

(8,482) |

| Profit for the year |

24,250 |

21,520 |

18,878 |

| Other comprehensive income for the year: |

|

|

|

| Items that will not be reclassified to profit or loss in subsequent period |

|

|

|

| Revaluation of property |

400 |

200 |

– |

| Total Comprehensive Income |

24,650 |

21,720 |

18,878 |

The draft statement of financial position as at December 31, 2016, is as follows:

|

Komolafe |

Kelvins |

Kelly |

| Non-current assets |

|

|

|

| Property, plant, and equipment (carrying amount) |

70,966 |

48,546 |

26,126 |

| Investments |

|

|

|

| Shares in Kelvins |

13,300 |

– |

– |

| Shares in Kelly |

– |

7,600 |

– |

| Total Non-current assets |

84,266 |

56,146 |

26,126 |

| Current assets |

3,136 |

18,050 |

17,766 |

| Total assets |

87,402 |

74,196 |

43,892 |

| Equity |

|

|

|

| Ordinary shares |

16,000 |

6,000 |

4,000 |

| Retained earnings |

45,276 |

48,150 |

39,796 |

| Current liabilities |

26,126 |

20,046 |

96 |

| Total equity and liabilities |

87,402 |

74,196 |

43,892 |

The following information is available relating to Komolafe, Kelvins, and Kelly:

- On January 1, 2012, Komolafe acquired 5,400,000 N1 ordinary shares in Kelvins for N13,300,000, at which date there was a credit balance on the retained earnings of Kelvins of N2,850,000. No shares have been issued by Kelvin since Komolafe acquired its interest.

- At the date of acquisition, the fair value of the identifiable net assets of Kelvins was N10 million. The excess of the fair value of net assets is due to an increase in the value of non-depreciable land.

- On January 1, 2014, Kelvins acquired 3,200,000 N1 ordinary shares in Kelly for N7,600,000, at which date there was a credit balance on the retained earnings of Kelly of N1,900,000. No shares have been issued by Kelly since Kelvins acquired its interest. The fair value of the identifiable net assets of Kelly at the date of acquisition approximates their book values.

- During 2016, Kelly made intra-group sales to Kelvins of N960,000, making a profit of 25% on cost. N150,000 of these goods were in inventories at December 31, 2016.

- During 2016, Kelvins made intra-group sales to Komolafe of N520,000, making a profit of 25% on sales. N120,000 of these goods were in inventories at December 31, 2016.

- An impairment test conducted at the year-end did not reveal any impairment losses.

- It is the group’s policy to value the non-controlling interest at fair value at the date of acquisition. The fair value of the non-controlling interests in Kelvins on January 1, 2012, was N1,000,000. The fair value of the 28% non-controlling interest (direct and indirect) in Kelly on January 1, 2014, was N1,800,000.

Required:

Prepare for Komolafe Group:

a. A consolidated statement of profit or loss and other comprehensive income for the year ended December 31, 2016. (13 Marks)

b. A consolidated statement of financial position as at December 31, 2016. (12 Marks)

c. In business combination, the consideration given by the acquirer to gain control of the acquiree can be in different forms, including deferred and contingent considerations. While deferred and contingent considerations represent amounts of consideration to be transferred in the future, the two differ in nature and form.

Required:

Briefly distinguish between deferred and contingent consideration. (5 Marks)

Total: 30 Marks