Question

Adeco Nigeria plc. is a large and diversified company with several factories. One of its factories that produces “Apet” has not been able to meet its sales target for over two years. The board has mandated the company’s management to take an urgent decision on what to do with the factory.

The management has therefore set up a committee of three, the factory manager, the marketing manager, and the management accountant to analyze the situation and come up with a report on what they felt the management should do. The marketing manager has submitted two proposals to the committee. These are:

- A sales volume of 25,000 units can be achieved with a selling price of N13.50 per unit and an advertising campaign of N37,500; or

- A sales volume of 35,000 units can be achieved at a selling price of N11.25 with an advertising campaign costing N52,500.

The management accountant is to work on these proposals with the information provided by the factory manager and show with calculations that will help the committee determine which proposal to be recommended to management. The management accountant is also to provide a third option, the closure of the factory.

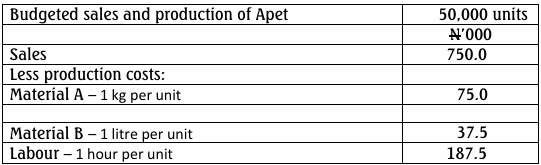

The factory manager has submitted the following information to the management accountant:

The following additional information has also been made available:

(i) There are 50,000 kg of material A in inventory. This originally cost N1.5 per

kg. Material A has no other use and unless it is used by the division, it will

have to be disposed of at a cost of N750 for every 5,000 kg.

(ii) There are 30,000 litres of material B in inventory. Any unused material can be

used by another department to substitute for an equivalent amount of a

material, which currently costs N1.875 per litre. The original cost of material B

was N0.75 per litre and it can be replaced at a cost of N2.25 per litre.

(iii) All production labour hours are paid on an hourly basis. Rumours of the

closure of the department have led to a large proportion of the department‟s

employees leaving the organisation. Uncertainty over its closure has also

resulted in management not replacing these employees. The department is

therefore, short of labour hours and has sufficient to produce only 25,000

units. Output in excess of 25,000 units would require the department to hire

contract labour at a cost of N5.625 per hour. If the department is shut down

the present labour force will be redeployed within the organisation.

(iv) Included in the variable overhead is the depreciation of the only machine

used in the department. The original cost of the machine was N300,000 and it

is estimated to have a life of 10 years. Depreciation is calculated on a straightline basis. The machine has a current resale value of N37,500. If the

machinery is used for production, it is estimated that the resale value of the

machinery will fall at the rate of N150 per 1,000 units produced. All other

costs included in variable overhead vary with the number of units produced.

(v) Included in the fixed production overhead is the salary of the factory manager

which amounts to N30,000. If the department were to shut down the manager

would be made redundant with a redundancy pay of N37,500. All other costs

included in the fixed production overhead are general factory overheads and

will not be affected by any decision concerning the factory.

(vi) The non-production cost charged to the factory is an apportionment of the

total non-production costs incurred by the factory.

The committee will be meeting in a week‟s time to prepare its report to

management on the line of action management should follow, either one of the

marketing manager‟s proposals or to close down the factory.

63

Required:

As the management accountant of Adeco plc., you are to:

a. Prepare detailed calculations to support the committee‟s recommendation to

the management whether to:

i. reduce production to 25,000 units

ii. reduce production to 35,000 units

iii. shut down the factory. (20 Marks)