- 15 Marks

AT – Nov 2016 – L3 – SC – Q5 – Tax Incentives and Reliefs

Identify industries qualifying as Pioneer Industries and compute tax liabilities and withholding tax for Ajanaku Nigeria Limited.

Question

a. **One of the incentives available to industries in Nigeria is contained in the Industrial Development (Income Tax Relief) Act 1971, which grants tax holidays to companies in the industries that meet the conditions for being designated “Pioneer Industries.”

Under the Industrial Development (Income Tax Relief) Act 1971, state any FOUR industries that qualify to be regarded as Pioneer Industries.** (4 Marks)

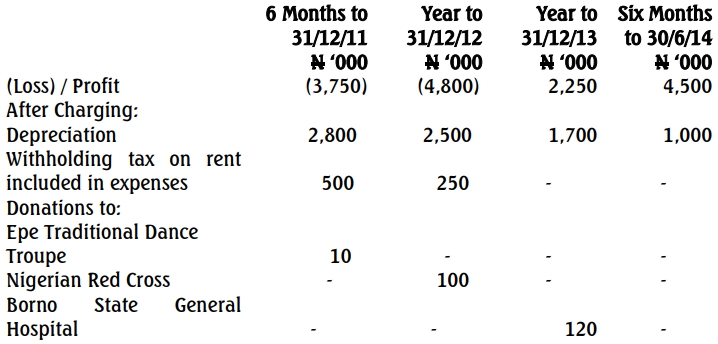

b. Ajanaku Nigeria Limited was incorporated as a pioneer company on March 15, 2011, with a focus on the manufacture of aluminum roofing sheets. It was granted a Pioneer Certificate with Production Day given as July 1, 2011. Extracts of Audited Financial Statements are as shown below:

| Period | 6 Months to 31/12/11 | Year to 31/12/12 | Year to 31/12/13 | Six Months to 30/6/14 |

|---|---|---|---|---|

| (Loss) / Profit | (3,750) | (4,800) | 2,250 | 4,500 |

| After Charging: Depreciation | 2,800 | 2,500 | 1,700 | 1,000 |

| Withholding Tax on Rent Included | 500 | 250 | – | – |

| Donations to: | ||||

| Epe Traditional Dance Troupe | 10 | – | – | – |

| Nigerian Red Cross | – | 100 | – | – |

| Borno State General Hospital | – | – | 120 | – |

Additional Information:

- Ajanaku Nigeria Limited declared gross dividends of ₦600,000 and ₦1,500,000 for 2013 and 2014, respectively.

- Withholding tax rates on dividends for the relevant years are 10%.

- Ignore minimum tax provisions.

- The company’s initial tax relief period was not extended.

Required:

Compute the tax liabilities for the relevant years of assessment relating to Pioneer Status only, and state the amount of Withholding Tax due from the shareholders. (11 Marks)

a. Four Industries Qualifying as Pioneer Industries:

- Agricultural production, including food processing and packaging.

- Manufacturing, such as aluminum products and roofing sheets.

- Mining and processing of minerals, including petroleum refining.

- Telecommunication and information technology.

b. Computation of Tax Liabilities and Withholding Tax for Ajanaku Nigeria Limited:

Step 1: Pioneer Period

- Pioneer period runs from July 1, 2011, to June 30, 2014.

Step 2: Loss/Profit Exemption During Pioneer Period

- Losses incurred during the pioneer period are disregarded for tax purposes.

- Profits during the pioneer period are exempt from tax.

Step 3: Dividend Withholding Tax (WHT):

| Year | Gross Dividend (₦’000) | Withholding Tax Rate (%) | WHT Amount (₦’000) |

|---|---|---|---|

| 2013 | 600 | 10 | 60 |

| 2014 | 1,500 | 10 | 150 |

Total Withholding Tax Due = ₦60,000 + ₦150,000 = ₦210,000.

Final Tax Liabilities:

- Since Ajanaku Nigeria Limited’s profits during the pioneer period are exempt from tax, Tax Liability = ₦0.

Withholding Tax Due from Shareholders:

- Total Withholding Tax on dividends for 2013 and 2014 is ₦210,000.

Find Related Questions by Tags, levels, etc.

- Tags: Pioneer Status, Tax computations, Tax Holiday, Withholding Tax

- Level: Level 3

- Topic: Tax Incentives and Reliefs

- Series: NOV 2016