Question

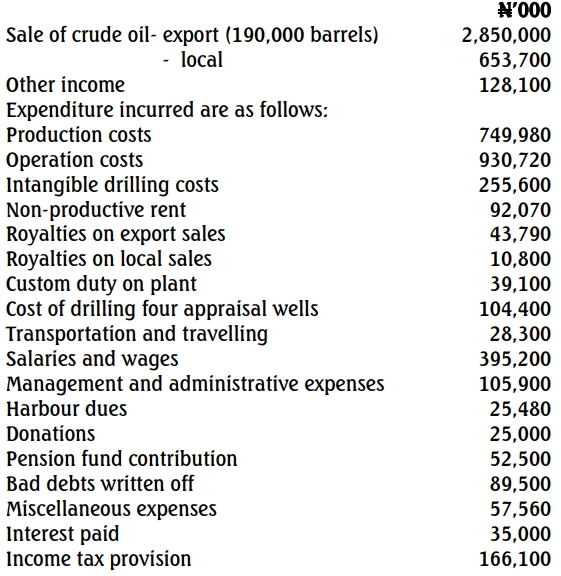

b. Priceless Oil Limited commenced crude oil production in Nigeria in 2006. The company has provided the following financial report for the year ended December 31, 2018:

Additional Information:

- Posted price for exported crude oil averaged $52/barrel (at an exchange rate of ₦306 to $1).

- Included in other income: ₦38,000,000 from crude transportation (cost: ₦16,250,000).

- Natural gas contract with Tommy Limited: value ₦655,000,000, load factor 54%.

- Depreciation of ₦120,250,000 was included in production costs.

- Qualifying capital expenditures:

| Type | Date | Location | Amount (₦) |

|---|---|---|---|

| Storage tank | March 12, 2018 | On-shore | 23,500,000 |

| Plant and equipment | November 15, 2018 | Continental Shelf of 130 metres of water depth |

75,000,000 |

- Capital allowances brought forward: ₦33,700,000; for the year: ₦88,500,000.

- Admin expenses include ₦3,500,000 stamp duties for debentures.

- Specific bad debts written off: ₦39,500,000.

- Donations were wholly expended for petroleum operations.

- ₦12,250,000 was paid to retrieve petroleum-related data (included in miscellaneous expenses).

- ₦20,500,000 interest was paid to an associate company at market rate.

Prepare and submit a report on the following computations:

i. Assessable profit (12 Marks)

ii. Chargeable profit (6 Marks)

iii. Chargeable tax (6 Marks)

iv. Total tax payable (6 Marks)