- 20 Marks

FR – Nov 2024 – L2 – Q1- Group Financial Statements

Preparation of the consolidated statement of profit or loss and statement of financial position for Yarkpawolo Group, including goodwill calculation and intra-group adjustments.

Question

Yarkpawolo LTD, a company in the healthcare industry, purchased 80% of the ordinary shares of Weah LTD on 1 January 2023. There are three elements to the purchase consideration: an immediate payment of GH¢1,400,000 and two further payments of GH¢100,000 on 31 December 2023 and GH¢120,000 on 31 December 2024 if the return on capital employed (ROCE) exceeds 15% in each of the financial years. All indicators have suggested that the ROCE for the company will be 17% and 16% for the financial years ending 31 December 2023 and 31 December 2024 respectively.

Yarkpawolo uses a discount rate of 10% in any present value calculations. The present value of GH¢ 1 receivable based on 10% are as follows:

| Year | Present Value |

|---|---|

| 1 | 0.909 |

| 2 | 0.826 |

The draft financial statements of both companies as at 31 December 2023 are as follows:

Statement of Profit or Loss for the year ended 31 December 2023

| Yarkpawolo (GH¢’000) | Weah (GH¢’000) |

|---|---|

| Sales revenue | 14,000 |

| Cost of sales | (10,000) |

| Gross profit | 4,000 |

| Operating expenses | (2,050) |

| Profit before tax | 1,950 |

| Income tax expense | (450) |

| Profit for the year | 1,500 |

| Retained earnings brought forward | 3,500 |

| Retained earnings to statement of financial position | 5,000 |

Statement of Financial Position as at 31 December 2023

| Yarkpawolo (GH¢’000) | Weah (GH¢’000) |

|---|---|

| Non-current assets: | |

| Property, Plant & Equipment | 4,500 |

| Patents | 500 |

| Investment in Weah | 1,400 |

| Total Non-current assets | 6,400 |

| Current assets: | |

| Inventories | 5,500 |

| Trade and other receivables | 2,000 |

| Cash and cash equivalents | 1,200 |

| Total Current assets | 8,700 |

| Total Assets | 15,100 |

| Equity: | |

| Share capital (GH¢0.20 per ordinary share) | 1,500 |

| General reserve | 3,000 |

| Retained earnings as at 31 December 2023 | 5,000 |

| Total Equity | 9,500 |

| Non-current liabilities: | |

| Long-term borrowings | 1,600 |

| Current liabilities: | |

| Trade and other payables | 4,000 |

| Current portion of long-term borrowings | – |

| Total Liabilities | 5,600 |

| Total Equity and Liabilities | 15,100 |

Additional Information:

-

Fair Value Adjustments on PPE:

- Property: Increase from GH¢200,000 to GH¢250,000 (Depreciation rate 10%)

- Plant: Increase from GH¢80,000 to GH¢100,000 (Depreciation rate 20%)

- Equipment: Decrease from GH¢120,000 to GH¢80,000 (Depreciation rate 20%)

- Weah has not adjusted its PPE values for the fair value assessment.

-

Intra-Group Trading:

- Since acquisition, Weah purchased GH¢50,000 worth of goods from Yarkpawolo. Half of these goods remained in inventory at year-end. Yarkpawolo makes a mark-up on cost of 25%.

- Yarkpawolo also purchased GH¢50,000 of goods from Weah, with one-third remaining in inventory. Weah sells at a margin of 20%.

-

Intercompany Balances:

- Yarkpawolo’s trade receivables include GH¢5,000 owed by Weah. The current accounts do not balance due to GH¢2,000 in transit from Weah.

-

Impairment:

- A goodwill impairment review identified a loss of GH¢100,000. No adjustment has been made yet.

-

Non-controlling Interest Valuation:

- Yarkpawolo values non-controlling interest at fair value at the acquisition date. The share price for Weah was GH¢0.75 per share.

Required:

Prepare for Yarkpawolo LTD:

(a) Consolidated Statement of Profit or Loss for the year ended 31 December 2023

(b) Consolidated Statement of Financial Position as at 31 December 2023

Find Related Questions by Tags, levels, etc.

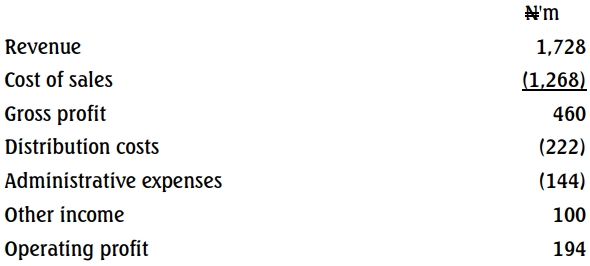

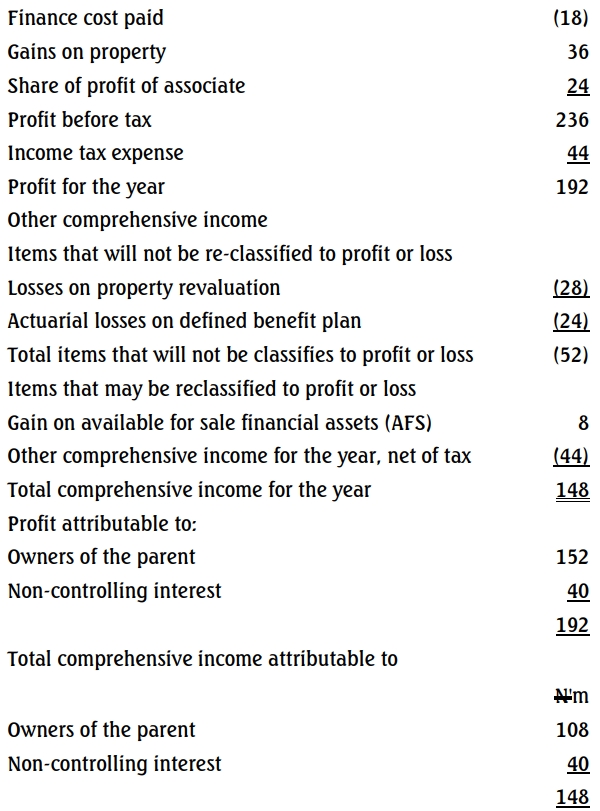

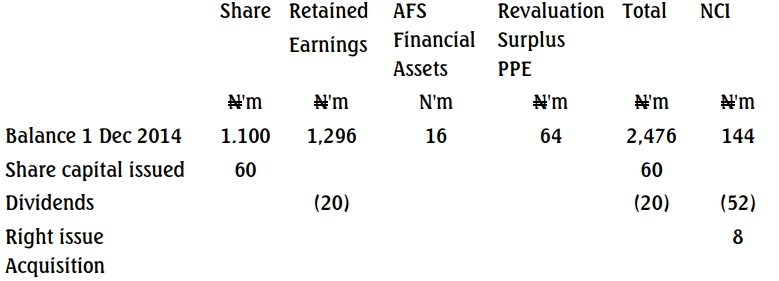

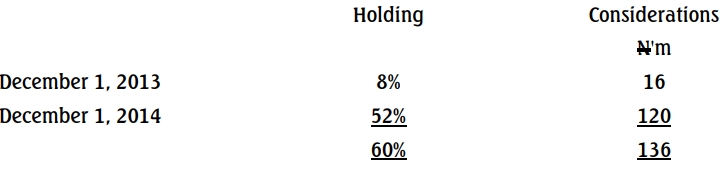

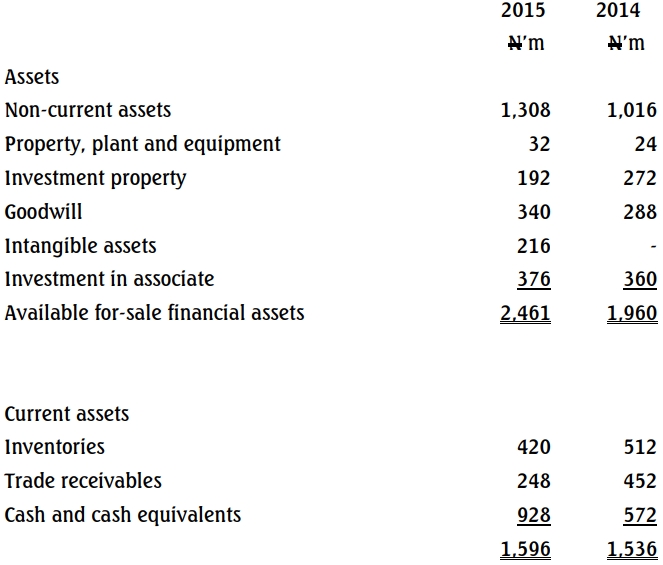

Joy-land Group: Statement of comprehensive income for the year ended November 30, 2015.

Joy-land Group: Statement of comprehensive income for the year ended November 30, 2015.