- 20 Marks

CR – Nov 2022 – L3 – Q3 – Impairment of Assets (IAS 36)

Evaluate impairment of a CGU for Evo Plc, considering fair value, cost to sell, and cash flows.

Question

Evo Plc acquired a cash-generating unit (CGU) several years ago. The directors of Evo Plc were concerned that the value of the CGU had declined because of a reduction in sales due to new competitors entering the market. At February 28, 2021, the carrying amounts of the assets in the CGU before any impairment testing were:

| Asset | Carrying Amount (N’m) |

|---|---|

| Goodwill | 3 |

| Property, Plant and Equipment | 10 |

| Other Assets | 19 |

| Total | 32 |

The fair values of the property, plant, and equipment and the other assets at February 28, 2021, were N10 million and N17 million, respectively, and their costs to sell were N100,000 and N300,000, respectively. The CGU’s cash flow forecasts for the next five years are as follows:

| Date (Year Ended) | Pre-tax Cash Flow (N’m) | Post-tax Cash Flow (N’m) |

|---|---|---|

| 28 February 2022 | 8 | 5 |

| 28 February 2023 | 7 | 5 |

| 28 February 2024 | 5 | 3 |

| 28 February 2025 | 3 | 1.5 |

| 28 February 2026 | 13 | 10 |

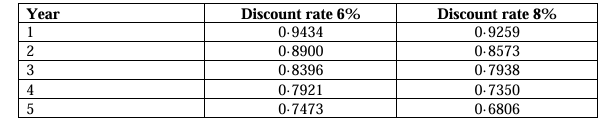

The pre-tax discount rate for the CGU is 8%, and the post-tax discount rate is 6%. Evo Plc has no plan to expand the capacity of the CGU and believes that a reorganisation would bring cost savings, but as yet, no plan has been approved. The directors of Evo Plc need advice as to whether the CGU’s value is impaired.

The following extract from a table of present value factors has been provided:

| Year | Discount Rate 6% | Discount Rate 8% |

|---|---|---|

| 1 | 0.9434 | 0.9259 |

| 2 | 0.8900 | 0.8573 |

| 3 | 0.8396 | 0.7938 |

| 4 | 0.7921 | 0.7350 |

| 5 | 0.7473 | 0.6806 |

Required:

a. How is impairment loss determined and accounted for by a business entity? (6 Marks)

b. Advise the directors of Evo Plc on:

i. Whether the CGU’s value is impaired. (7 Marks)

ii. How the transactions above should be treated in its financial statements in accordance with the provisions of IAS 36 – Impairment of Assets. (7 Marks)

(Total 20 Marks)

Find Related Questions by Tags, levels, etc.

- Tags: Cash-Generating Unit, Fair Value, Financial Reporting, Impairment, Value in Use

- Level: Level 3

- Topic: Impairment of Assets (IAS 36)

- Series: NOV 2022